|

|

|

|

|

|

| Topics >> by >> irs_foreign_earned_income_ex |

| irs_foreign_earned_income_ex Photos Topic maintained by (see all topics) |

||

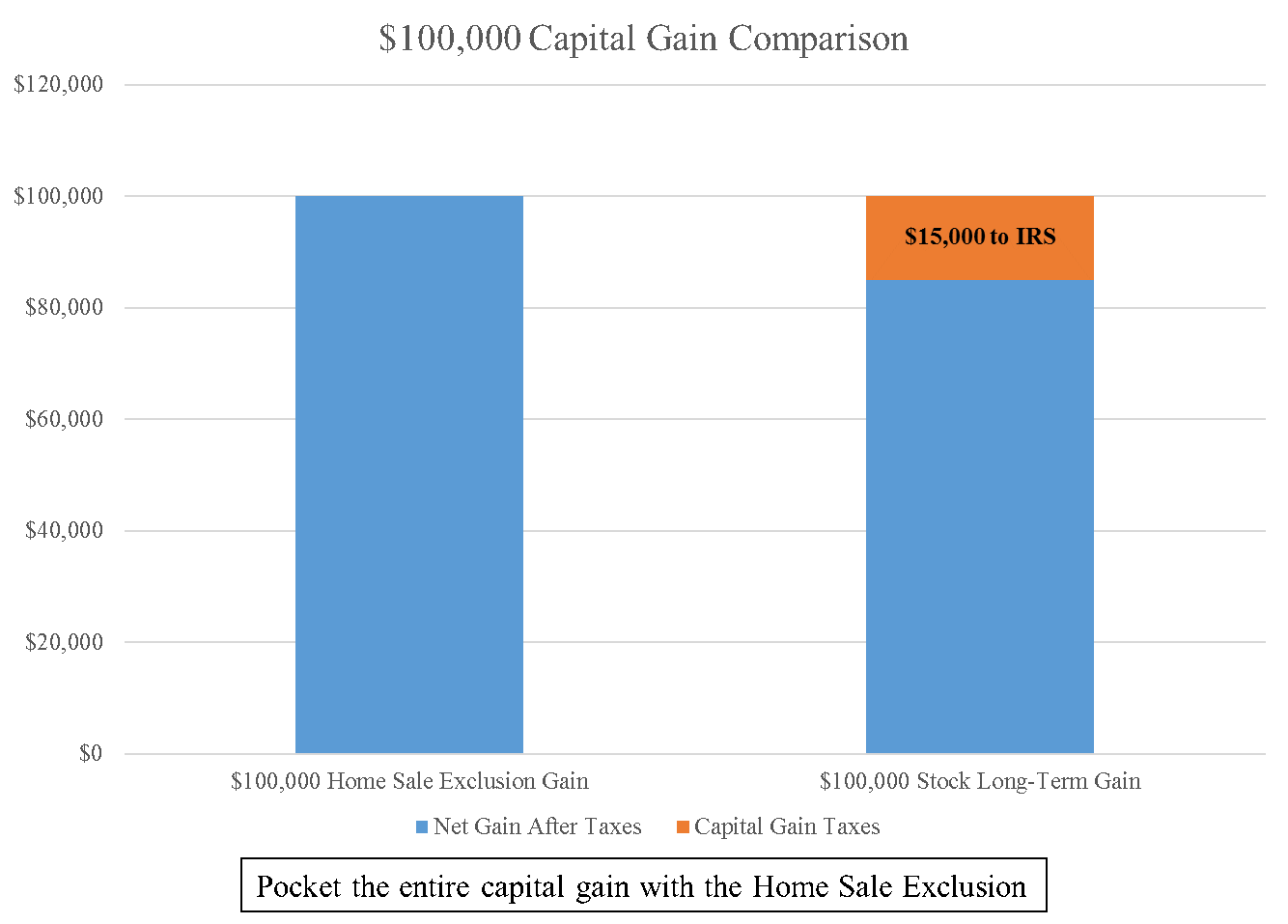

The Ultimate Guide To How to get an IRS home sale exclusion when earning profit onTherefore, Nancy and Oscar will exclude $225,000 from the sale of Nancy's house and $250,000 from the sale of Oscar's home. Because Oscar can not utilize any of Nancy's unused exclusion, the couple needs to consist of $25,000 of the gain on his house in earnings. Animal Removal would be the same if Nancy and Oscar each had actually sold their houses before marrying. If the couple then move into the home that could produce a gain in excess of $250,000 and live there for at least two years, the couple would qualify for the $500,000 exemption as long as that sale does not take place within 2 years of the first sale. In the above example, if Nancy and Oscar offer Nancy's house and reside in Oscar's house for at least two years prior to offering it, the whole $275,000 gain would be omitted from income if your house is cost least two years after the sale of Nancy's home.  Further, if the making it through partner has not remarried, both the departed partner's ownership and usage as a principal residence are associated to the survivor. Peter and Quill, a couple, have actually owned and used their home as a primary residence considering that 1998. Peter passes away on June 1, 2002. On November 1, 2002, Quill sells the home at a $280,000 gain. The Greatest Guide To The Home Sale Exclusion and current events - The CPAIf, however, Quill sells the home on January 10, 2003, only $250,000 of the gain is eligible for the exemption because Peter and Quill can not submit a joint return in 2003. If a decedent was the sole owner of a house, the residential or commercial property's basis will be its fair market worth at the date of death.  If the home is owned jointly, the basis of the decedent's half of the home is its fair market value at the date of death. The increase in value on that half of the home gets away income tax, and sale of the house in the year of death matters only if the surviving partner's share of the increase in worth exceeds $250,000. |

||

|

||