the_wrong_life_insurance_pol Photos Topic maintained by (see all topics)

Content author-Vendelbo Sears

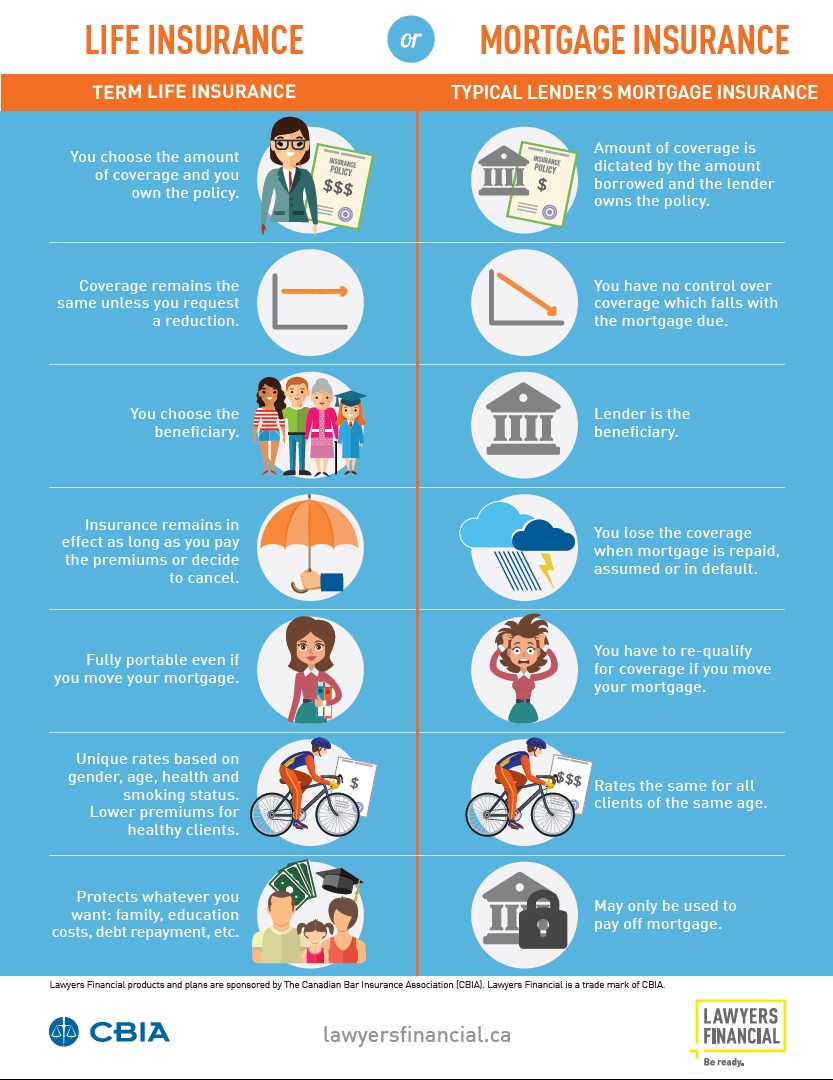

Life insurance is not easy to shop for. There are so many providers and so many options that it is all too easy to get lost. A little research can equip you to find your way. This article will present a few handy tips to keep you on the right track to good life insurance deals.

When creating a divorce settlement that requires one parent to maintain life insurance in order to keep custody of children, create the insurance policy before signing the divorce settlement. Read the Full Report speeds up the settlement process and insures that any kinks in the making of the insurance policy are dealt with before the custody issues.

When considering life insurance, it is best to buy it as soon as possible in your career. Rates will only go up as you get older, and with the addition of other ailments that you might be diagnosed with you may not even qualify for coverage. Start as early as you can and try to lock in a low rate.

Choose the life insurance amount wisely. The older you are and the larger the payout, the more it costs. Keep in mind: life insurance is not designed to pay off your house and finance your whole family for the rest of their natural lives. Choose an amount which comfortably helps them through the few month after your death.

Buy the right amount of life insurance to cover all of your needs. Skimping on life insurance is not a good idea. Term insurance, especially, is very affordable, so make sure you get as much insurance as you need. For a rule of thumb, consider buying insurance that equals approximately 6 to 10 times your income.

Choose permanent life insurance if you want to build cash value. Building cash value in a life insurance policy helps you have additional cash for the future. The insured can borrow the cash value at a low interest rate. They can also use it to pay the premiums. The cash grows tax-free, and some financial planners recommend it as a way to cover estate taxes as part of a comprehensive financial plan.

Most life insurance companies require you to take a medical exam before they give you coverage. They look at blood pressure, cholesterol levels, an EKG of your heart rate activity, and many other indicators that reveal the presence of any type of disease or risk factors. You can perform better on the test, even put yourself into a higher rate class, by eating low-fat foods for the two days before your test. Drink extra water to maintain hydration, and avoid alcohol for three to four days ahead of the test. Also, make sure you get plenty of sleep for the week leading up to the exam.

Get yourself a policy that has a "conversion to permanent" clause. This refers to the fact that at any time, the policy holder can switch their term insurance into permanent insurance without further medical exams. While this may not save money at first, it will eventually save money if you start suffering from poor from health problems before the policy runs out.

You do not have to enroll in a policy that gives you a huge amount. This is not necessary because of their high cost while you are alive. Instead, purchase a policy that is just enough to cover your family's expenses if you die.

It's important that you understand that term life insurance is only for protection and not for investing. There is no savings component in term life insurance, so your best bet here is to simply pay for this type of insurance and invest elsewhere. Your policy payments aren't collecting interest or anything.

If you want to have some control and decision-making power over the money you invest in your life insurance, consider a variable, universal life insurance policy. With these policies, you have the ability to invest part of your premium in the stock market. Depending on how wisely you invest this portion of your money, your death benefit can increase over time. You should have some knowledge of the stock market if purchasing this type of policy or enlist the aid of a financial professional.

Don't be tempted to lie or hold back information on your application for life insurance. If you have medical issues or other possible rate hikers, your company will investigate any time you file a large claim. This means they will find the hidden truth and can revoke your policy.

If you do not have any major health problems, do not go with guaranteed issue policies. Getting https://drive.google.com/file/d/1J4DLOgXcY70ZxTgoKIMRBoSbdNmKQDVu/view?usp=sharing will save you money, and the guaranteed issue policies do not need that, and has higher premiums. You don't need to spend more on life insurance than is really needed.

If you have minor children, purchase enough life insurance to offset their expenses until adulthood. The loss of your income could have a significant impact on your children's lives, and life insurance can help close the financial gap. This affects not only day-to-day expenses, but also those larger ones like college costs.

You should forget about cliches regarding life insurance. Life insurance is the butt of many jokes about greedy relatives waiting for an elderly person to die so that they can get insurance money. You should see life insurance as a way to help your relatives and not burden them any further with the expenses related to your death or medical condition.

Be honest when you fill out the application for life insurance. It is crucial that you do not lie on your forms; insurance companies have the right to cancel your policy if they find out that you were dishonest. It would probably be more beneficial just to buy an additional policy.

Life insurance is a part of financial planning which protects your loved ones when the worst occurs. After a tragedy occurs, peace of mind in any form is very beneficial to your loved ones.

With life insurance it's all about finding the right type of insurance. There's term life insurance, whole life insurance, universal life insurance, and variable life insurance. Each have their positives and negatives and it's good to research or talk to an agent about which type would be the best fit for you and your family. All insurance plans should be individualized to meet your desires.

When purchasing life insurance, understand how much coverage you may need. A good rule of thumb commonly recommended is coverage for between 5 and 10 year's worth of your income. Go closer to 5 if you have few dependents and little debt, and more toward 10 if you have many dependents and lots of debt.

As you can see from the above list of tips, choosing a life insurance policy can be very helpful when trying to decide on what coverage that you and your loved ones need. After following these tips, you will no longer be new to life insurance policies, but you can become more knowledgeable about it.

has not yet selected any galleries for this topic.