|

|

|

|

|

|

| Topics >> by >> The 10 Scariest Things About transact-online |

| The 10 Scariest Things About transact-online Photos Topic maintained by (see all topics) |

||

| Ultimately - banking modern technology and also big information are high up on the agenda for economic solutions C-suites. Financial leaders identify that the ability to essence as well as use data held within their service operations - and also to automate file procedures in their worth chain, offer incredible competitive advantage. At the same time, as open financial becomes a fact of life for both customers and financial institutions, it introduces new avenues for developing income streams. Nevertheless, in several organisations, there are barriers obstructing those possibilities. Occasionally it's budgetary restraints; various other times, it's merely a lack of assistance and/or understanding across business. Here are 5 pushing reasons to re-prioritise smart record processing (IDP) in your digital makeover program, and knock down those barriers one at a time. 1. Big information in financial is a significant, unmissable chance

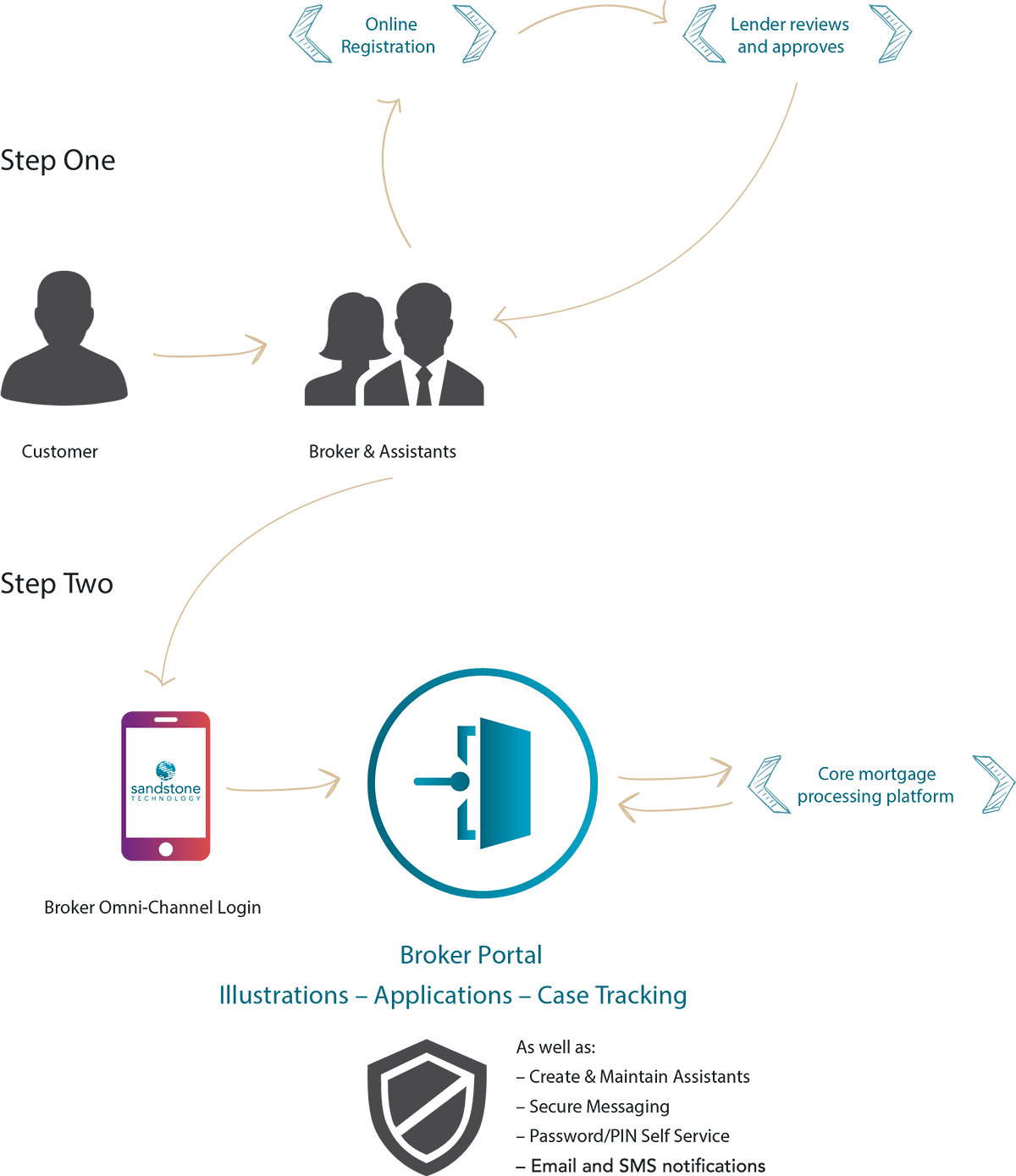

As challenger financial institutions continue to disrupt the financial solutions landscape, typical banks have one wonderful advantage-- the substantial amounts of data they hold associating with their customer bases as well as sectors. Lending applications alone generate hills of data to satisfy back-end procedures. But this information isn't constantly in a kind that can be accessed; nor is it confirmed for its stability. Being able to instantly translate client papers for smart understandings opens beneficial information for banks, which can after that be fed into other areas of business, or into applications. From there, banks can establish items to satisfy the demands of retail, SME as well as commercial customers and also dissolve their discomfort points; they can improve the customer experience, as well as make it possible for financial health and wellbeing conversations in between customers and also the market. Data powers personalisation, opening communication with clients regarding items at the right time, in a way that makes sense to individuals. Consumer data comes to be a resource to shape method. IDP utilizes a collection of innovations - from expert system (AI) as well as machine learning (ML) to optical character recognition (OCR) and also natural language processing (NLP). These allow banks to record, identify, as well as extract information kept in papers, transforming unstructured as well as semi-structured information right into a structured format. Smart automation technology can after that be applied to the drawn out information for improved validation and to automatically enter it right into existing applications. Advanced analytics allow for reporting and insights in real time from numerous sources, so organisations can take in, evaluate and also carry out on the understandings, feeding into the financial institution's worth proposal. 2. The COVID effect: brand-new assumptions from end consumers With social distancing limitations, lockdowns and also a mass work-from-home motion in many markets, we've seen a change in consumer interaction. It started with a mass flight to digital channels throughout both retail and also commercial financial, accompanied by increasing download rates for apps, especially in the early months of the pandemic. " The banks are now reprioritising their digital makeover programs," states Sandstone Innovation CEO Michael Phillipou. " 18 months earlier, a bank may have had a roadmap of 3 years of programs they were mosting likely to be resolving. Currently they realise they need to increase that financial investment, reprioritise some of those programs, as well as generate new concerns to guarantee they've got market-leading electronic value proposals." " This rate and also dexterity is something we have actually never seen before," Phillipou claims. Overnight, digital services have actually been established to meet clients' need for safety and security and comfort, and also cashless payments and international settlements have became a must. " We also unexpectedly saw a need for instant gratification," says Phillipou. "Getting answers swiftly and also having the ability to interact with your bank, either by self service or by a lender beyond, are now expected as a matter of course." Keep in mind that in an atmosphere of online banking solutions inc enhancing cybersecurity violations, new banking technology needs to be stabilized with conformity, information safety and security as well as risk monitoring. "If repayment systems were to decrease, that would have a tragic result economically and destroy trust in establishments," Phillipou states. 3. Digital borrowing options will certainly always have hefty compliance commitments Financial institutions have a conventional profile and rightly so. They have substantial and also ever-changing regulative responsibilities to stick to, and layers of stakeholder approvals to secure before onboarding any type of brand-new capabilities. " Therefore, recognized financial institutions normally aren't technology leaders," Philippou states.

Nevertheless there is a huge possibility for financial institutions to enhance their capacity to fulfill regulative compliance promptly as well as conveniently-- via automated IDP products like Sandstone's DiVA. DiVA gives customers shown and also auditable governing conformity via an built-in rules engine without any code arrangement needed. As well as because DiVA is Software Application as a Service, it's rapid to carry out. A financial institution might possibly set up IDP throughout their company in a issue of weeks. " This is what financial innovation will certainly appear like across the board in the future," Phillipou claims. "Cloud native, cloud based, API initially, containerised, with microservices-- all of these together make it possible for fast implementation and also rapid realisation of benefits. Being consumption based, the item can be activated and also off rapidly." 4. The drive for efficiency gains across the board According to Phillipou, from the bank's point of view, every board is being asked to do three points. The initial is to raise their return on capital, which indicates expanding their possessions, their financing publications and also obligation books. The 2nd: they require to currently do even more with much less, by lowering their cost-to-income proportion. And ultimately, number three is to follow all guidelines as well as prevent fines. " When it come to the second factor, this is definitely an performance play," Phillipou states. "The right electronic loaning option will certainly cause lowered time to refine lendings, which's the major usage case our clients are using our capability for. Smart document processing is a vital part of that." With smart automation, financial institutions can begin to provide loans out to customers at a much better speed than they could have or else. Personal info can be redacted, papers can be rotated and interpreted and indexed. And with even more precision in the method they process information, and also little or no re-keying of info, the error rate with customers is far reduced. As the procedure becomes a lot more efficient for organisations, they can redeploy those back-office sources right into various other locations where they can get a higher influence. It has to do with expense savings for customers as well as a far better consumer experience with fewer discomfort factors. Ultimately banks are working towards the concept of right via handling (STP): absolutely electronic processing of financial transactions from the point of very first ' bargain' to final settlement, including no manual intervention. The goal is to accomplish far better rate, precision, integrity and scalability. 5. The open financial future counts on good, huge data in financial The staged introduction of open financial as well as the opening of APIs to 3rd parties has been an additional catalyst for change, helping change sector emphasis onto the significance of information integrity and also ease of access. Financial institutions require to be able to seize the opportunities this provides. That consists of opening ' industries' to aid develop out their very own item collection and also check out brand-new revenue streams for the business. These could include anything from re-selling to economic understandings for retail as well as company financial. As Philippou states, "From our side, as a technology partner, we're seeing far more requests for remedies to fulfill these requirements today." There is no doubt that banks should be data driven if they want to give far better financial services and products to fulfill consumers' needs and also expectations; and if they wish to take advantage of possibilities as they develop. At the same time, they require to drive performance and effectiveness across business, while reducing operational danger. The time has actually pertained to adjust, and do it quickly. |

||

|

||